Global Equities

Categories

Asset Allocation

2023 market trends in 5 charts

This year has been full of surprises, prompting investors to reset their expectations more than once.

In January, the mood was solemn as markets were still recovering from 2022’s sharp decline, and a recession felt inevitable. But then an AI-fueled tech rally lifted the U.S. stock market, while returns in Europe and Japan proved to be stronger than expected. The lesson? Market surprises should not be surprising.

What’s next for investors as we grapple with higher-for-longer interest rates and slowing-but-persistent inflation? Here are five of the most important trends to watch as the year unfolds:

1. A rolling recession may have already begun

Many economists predicted an imminent recession when the U.S. Federal Reserve first increased interest rates more than 18 months ago. Eleven hikes later, a broad economic downturn hasn’t materialized.

But what if the recession already happened? Just not all at once.

A rolling recession occurs when industries rise and fall at different times, creating pain in certain sectors while others flourish. For example, the travel and energy sectors cratered in 2021, but have since rebounded strongly. Likewise, housing and semiconductor stocks slumped in late 2022 before picking up in recent months.

In such an environment our portfolio managers seek to take advantage of these “mini-recessions” by looking for potential opportunities in industries on the rebound, rather than focusing too much on the timing or magnitude of a broad recession.

Different sectors have experience downturns at different times

Sources: Travel: Capitals Express Investments, Transportation Security Agency (TSA), U.S. Department of Homeland Security. Data is a 30-day moving average. As of July 26, 2023. Semiconductors: Capitals Express Investments, Philadelphia Stock Exchange, Refinitiv Datastream. As of June 30, 2023. Data represents cumulative price return in USD since January 1, 2019. Housing: Capitals Express Investments, Refinitiv Datastream, Standard & Poor's. Latest available monthly data is May 2023, as of July 27, 2023. Manufacturing: Capitals Express Investments, Institute for Supply Management (ISM), National Bureau of Economic Research. Refinitiv Datastream. Figures reflect the seasonally adjusted survey results from ISM's Manufacturing Purchasing Managers’ Index (PMI). A PMI reading above 50 percent indicates that the manufacturing economy is generally expanding; below 50 percent indicates that it is generally declining. As of June 30, 2023. Chemicals: Capitals Express Investments, U.S. Federal Reserve, Refinitiv Datastream. Data indexed to 100 in 2017. Figures are seasonally adjusted. As of June 30, 2023. Oil: Capitals Express Investments, Refinitiv. As of July 26, 2023. Past results are not predictive of results in future periods.

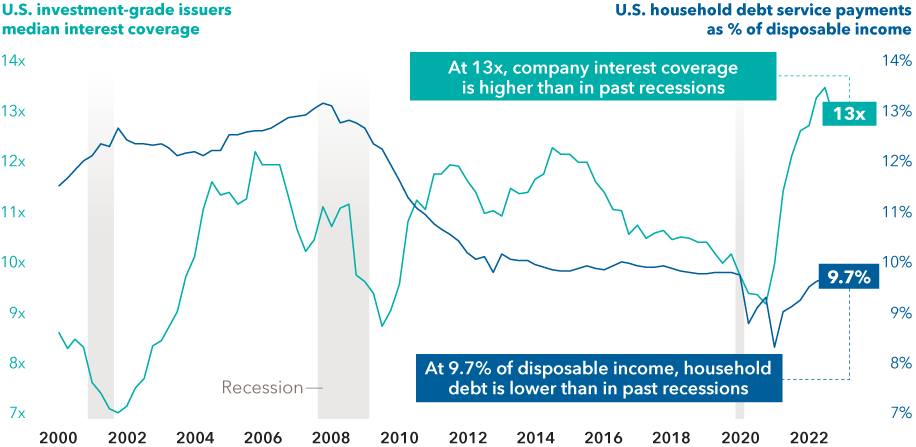

2. Resilient consumers could lead a strong economic recovery

Whether a rolling recession is already underway or a more traditional one is on the horizon, many investors are wondering what’s next.

The good news is that there are several reasons an eventual recovery could be relatively strong.

For one, the U.S. consumer appears to be in relatively good shape. Household debt was only 9.8% of disposable income as of June 30, 2023 — much lower than during the global financial crisis and other typical recessions. Supported by a strong labour market, resilient consumer spending could boost a range of industries including travel and leisure.

Secondly, a number of U.S. companies have cleaned up their inventories and balance sheets. The average interest coverage ratio — a measure of earnings over interest payments — is higher than it was during the past three recessions.

These factors combined could paint an optimistic long-term picture for investors during this period of uncertainty.

Consumers put their houses in order as companies cleaned up balance sheets

Sources: Capitals Express Investments, Federal Reserve Bank of St. Louis, Morgan Stanley, National Bureau of Economic Research. As of March 31, 2023.

3. Mountain of cash could be a bullish sign for investors

One of the most notable trends of the year has been investors’ flight to cash and cash equivalents. Money market fund assets in the U.S. ballooned to a record US$5.6 trillion as of September 27, according to the Investment Company Institute.

Our analysis reveals that levels of cash have tended to peak around market troughs and shortly before market recoveries. The S&P 500 Index surged after both the global financial crisis and COVID-19 pandemic, returning at least 40% in U.S. dollar terms within three months of each market bottom.

Investors who stayed on the sidelines would have missed these market recoveries, potentially impacting their ability to achieve their long-term goals.

Investors' flight to cash has been followed by strong returns

Sources: Capitals Express Investments, Bloomberg Index Services Ltd., Investment Company Institute (ICI), Standard & Poor’s. As of May 26, 2023. Past results are not predictive of results in future periods. Returns are in USD.

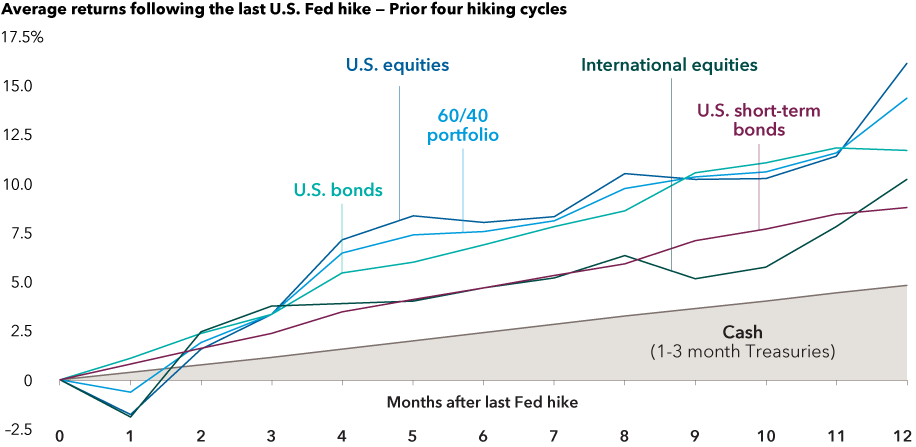

4. There have been windows of opportunity between a Fed pause and cut

While many investors may be planning to remain on the sidelines until the Fed starts cutting rates, our research shows that could be a mistake.

That’s because there have been windows of opportunity between the Fed’s last rate hike and first cut. We looked at asset class returns in the year after the Fed stopped hiking rates across the last four cycles. Our analysis revealed that cash had the lowest average returns during such periods, soundly outpaced by stocks, bonds and balanced portfolios.

In these instances, the first interest rate cut has been, on average, 10 months after the final rate hike. Investors who wait too long risk missing out on potential gains. Although the central bank’s most recent projections signaled one more rate increase before year-end, it appears the Fed is nearing the end of its current hiking cycle.

After Fed hikes ended, long-term results outpaced cash, with the first year contributing most

Sources: Capitals Express Investments, Morningstar. Chart represents the average returns across respective sector proxies in a forward extending window starting in the month of the last Fed hike in the last four transition cycles from 1995 to 2018 with data through 6/30/23. The 60/40 blend represents 60% S&P 500 Index and 40% Bloomberg U.S. Aggregate Bond Index, rebalanced monthly. Long-term averages represented by the average five-year annualized rolling returns from 1995. Past results are not predictive of results in future periods. Returns are in USD.

5. Bull markets have dominated bear markets

Bulls defeat Bears, 67 to 12. While that might sound like the lopsided score in a sporting event, it highlights an important fundamental truth about the stock market.

Our analysis of U.S. market cycles since 1950 revealed that while the average bear market has lasted 12 months, the average bull market has been more than five times longer.

The difference in returns has been just as dramatic. Even though the average bull market has had a 265% gain (versus a 33% decline for the average bear market), recoveries are rarely a smooth ride. Investors often face unsettling headlines, significant market volatility and additional equity declines. But those able to move past the noise, take a long view and stay invested through market cycles stand a better chance of scoring long-term gains.

Every bull market has been longer than the bear market that preceded it

Sources: Capitals Express Investments, RIMES, Standard & Poor’s. Includes daily returns in the S&P 500 Index from 6/13/49–6/30/23. The bull market that began on 10/12/22 is considered current and is not included in the “average bull market” calculations. Bear markets are peak-to-trough price declines of 20% or more in the S&P 500. Bull markets are all other periods. Returns are in USD and are shown on a logarithmic scale. Past results are not predictive of results in future periods.

Learn more about

Our latest insights

-

-

Artificial Intelligence

-

Technology & Innovation

-

-

Demographics & Culture

RELATED INSIGHTS

-

Global Equities

-

-

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

This content is confidential and designed for the exclusive use of registered dealers and their representatives. Canadian securities legislation, including National Instrument 81-102, prohibits its distribution to investors, potential investors or the general public. It is not intended to be a sales communication, as defined in the Instrument, and has not been designed to comply with its requirements relating to sales communications.

Unless otherwise indicated, the investment professionals featured do not manage Capitals Express Investments‘s Canadian mutual funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capitals Express Investments. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capitals Express Investments or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. We assume no liability for any inaccurate, delayed or incomplete information, nor for any actions taken in reliance thereon. The information contained herein has been supplied without verification by us and may be subject to change. Capitals Express Investments funds are available in Canada through registered dealers.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capitals Express Investments. Copyright © 2023 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2023. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

MSCI does not approve, review or produce reports published on this site, makes no express or implied warranties or representations and is not liable whatsoever for any data represented. You may not redistribute MSCI data or use it as a basis for other indices or investment products.

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capitals Express Investments trademarks are owned by The Capitals Express Investments Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capitals Express Investments funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capitals Express Investments, a global investment management firm originating in Los Angeles, California in 1931. Capitals Express Investments manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capitals Express Investments funds offered on this website are available only to Canadian residents.