Global Equities

Categories

Artificial Intelligence

AI and the new megacycle for tech

Julien Gaertner

Julien Gaertner

Drew Macklis

Drew Macklis

Mihir Mehta

Mihir Mehta

July 25, 2023

Too busy to plan your next business trip? Imagine this scenario: You set a date and destination in your digital calendar and then a bot powered by artificial intelligence (AI) does the rest. It searches for the cheapest flight that complies with your employer’s work travel policies, picks your preferred aisle or window seat, pays for the ticket, and adds it to your calendar.

Science fiction? This reality may not be too far in the future.

Given the vast potential of AI, it’s no surprise the market has sought to sniff out early winners and losers. Many technology stocks have soared since ChatGPT captured the public’s imagination earlier this year.

We believe this is the start of the next megacycle for the technology sector. But it won’t be linear, and investors will need to be nimble. Stock prices will likely go through fits and starts, with stocks getting overextended at times and pulling back when the market doubts progress.

There are also outstanding questions about AI’s impact on society and how best to regulate its development. With that in mind, here are six unfolding themes we are tracking that have potential impacts on companies and markets.

1. This tech cycle has important differences from previous ones

In several respects, AI is going to be different than previous technology cycles, whether it was mainframe computing, broadband internet or cloud computing. The big incumbents possess many first-mover advantages to deploy AI at massive scale. Large tech companies already have proprietary data, massive amounts of capital to spend and some of the brightest engineering talent. Some of them also own the very expensive cloud computing infrastructure necessary for training AI models.

Another advantage for the likes of Microsoft, Google and Apple is their large user bases to sell AI products and services to. While we expect some AI startups may find dramatic success over time, the starting point for incumbents is strong.

Importantly, the AI cycle appears likely to move fast. Take cloud computing as a comparison. That cycle began around 2008, and more than a decade later we estimate roughly 30% of corporate workloads are in the cloud. This is in large part because replacing existing architecture is a complex and time-consuming process.

AI is very different. It can simply be additive in some cases. For example, if a software vendor adds AI functionality to an existing product, it could be deployed in days or weeks — not years. Therefore, it will be key for big tech incumbents to be able to adapt quickly as the technology progresses.

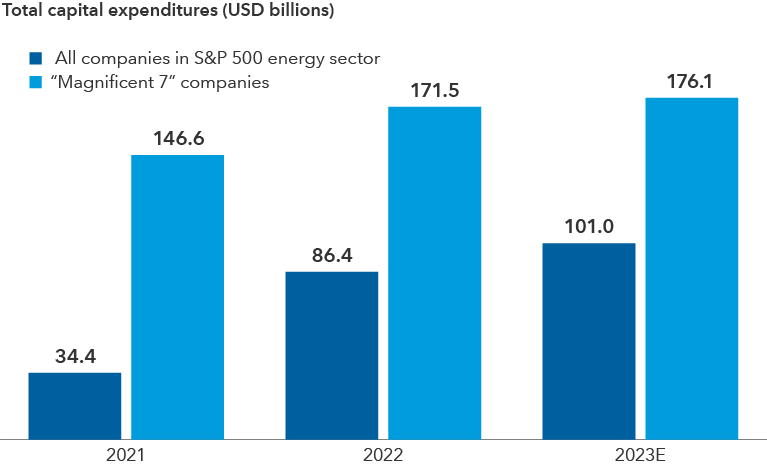

Leading tech companies are spending far more than the capital-intensive energy sector

Sources: Capitals Express Investments, FactSet, Standard & Poor's. Companies in the "Magnificent 7" reflect the top contributors in the S&P 500 year to date as of June 30, 2023, and include Apple, Microsoft, Alphabet, Amazon.com, NVIDIA, Tesla and Meta. Contribution to the S&P 500's total return is based on individual stock return performance multiplied by each constituents' weight in the index at the beginning of the period. Periods reflect calendar years, and figures for 2023 are forecasted based on the mean analyst estimates for capital expenditures across each company. As of July 18, 2023. E = estimated.

2. Speed and thoughtfulness of AI adoption can create differentiation

We believe that the speed of adoption of AI can create a competitive advantage for some companies. Put another way: If there are two firms that compete against each other today, and one company embraces AI holistically and early while the other doesn’t, we believe this could drive very different long-term business outcomes.

For example, companies that thoughtfully implement AI by making changes in areas such as research and development, product design and logisticscould see benefits in their margin structures, product development cycles and customer satisfaction scores.

High-quality management execution will also be crucial. The range of outcomes for all businesses has expanded substantially with this technology, and a premium will be placed on management teams that are forward-thinking, thoughtful and proactive. In our recent company meetings in Silicon Valley, we heard firsthand how venture capitalists are seeking to identify public companies whose leadership teams appear behind in implementing AI strategies so that they can back startups to disrupt them.

The global AI market is projected to reach nearly US$2 trillion by 2030

.png)

Sources: Next Move Strategy Consulting, Statista. Years 2023 through 2030 are estimated. Lighter blue boxes represent estimates. Data as of January 2023. CAGR = compound annualized growth rate. Dollar values in USD.

3. While AI offers a lot of opportunity, it also poses disruptive threats that companies are navigating

History has shown that simply trying to bolt on new technology to an existing business model can be problematic. Consider U.S. book retailer Barnes & Noble. Although the company had a website, its core business remained focused on physical stores. This limited its ability to compete in the digital age against online-native competitors like Amazon.com. As a result, Barnes & Noble’s market value plummeted. This lesson is particularly relevant now as AI has the potential to transform industries in unforeseen ways.

Online education firm Chegg is a recent case study taking place in real time. Its shares plunged 48% on May 2 after the company indicated that ChatGPT hurt its customer growth rate. In response, Chegg plans to launch a new tool with OpenAI, called CheggMate which will blend ChatGPT’s AI technology with Chegg’s educational services platform.

From our perspective, companies that own an exclusive set of data could be better positioned to strengthen or defend their businesses against competitors, especially if the data is hard to replicate and can be used to train large-scale AI models.

Adobe’s large stock photo library comes to mind, for example. The company may be able to use this library to train and fine-tune its algorithms. And importantly, unlike potential competitors, Adobe in our view may not run into copyright infringement problems on the images generated from those algorithms.

The tech giants will likely have to play some offence and defence. AI may change consumer engagement with web search for example, which is a huge profit centre for Google. Microsoft has been piloting versions of its flagship software programs (Word, Excel, PowerPoint and Teams) with AI functionality, known as 365 Copilot. And recently, Microsoft announced its business pricing strategy for Copilot, sending its shares intraday to an all-time record high.

4. The breadth of investment opportunities spans up and down the value chain

The investment cycle for AI has – and should continue to – produce early winners. But other beneficiaries across the value chain are also likely to emerge over time.

Underpinning the AI application layer is a critical set of infrastructure for training and deploying the models. Since AI requires tremendous computing power, some semiconductor companies are well positioned to benefit, particularly those that design chips that are the computational engines and backbone of AI. These would include graphic processing units (GPUs) as well as custom-built chips, called ASICs (application-specific integrated circuits).

NVIDIA, for instance, soared past US$1 trillion in market value after making bullish comments in May about potential revenue from demand for its processors used in AI computing. Other tech companies like Google, Amazon, Meta and Tesla have also been designing their own specific AI chips as they seek to explore supplements to Nvidia’s chips in a highly supply-constrained environment for AI processors. Demand should also grow for less discussed types of chips like networking and memory.

A wide range of potential end-industry applications is also likely to emerge.

In the field of radiology scans, for example, AI could be used to look at every scan globally and discover cases that may have not been previously identified in certain regions. Generative models might also be able to shorten the drug discovery process by identifying novel compounds of interest. Food production, with its many variables such as fertilizer usage, planting cycles and animal feed, is ripe for an AI-powered system that can cut costs while potentially increasing yields.

While it is early days in the diffusion of this new tech platform, the possibilities are expansive.

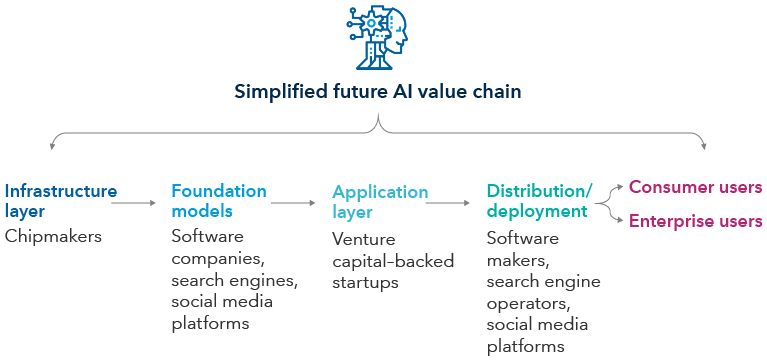

The potential value chain and investment opportunities

Source: Capitals Express Investments.

5. A nascent app ecosystem is developing around AI foundation models

When the iPhone was launched in 2007, Apple’s App store had a limited number of offerings. Now it's home to millions of apps, giving users a wide assortment of tools and services that were unimaginable before the iPhone. From being able to order an Uber from your phone, send a video on Snapchat, or pay with Apple Pay, the iPhone led to the creation of a vast ecosystem that generated US$1.1 trillion in developer billings and sales in 2022.

A similar moment is taking shape with ChatGPT, which now has plug-ins that can be thought of as the equivalent of an app store. This powerful new functionality on top of OpenAI’s core model enables it to gain new abilities like ordering groceries on Instacart, exploring travel bookings on Expedia or checking restaurant reservations on OpenTable.

Our expectation is that we will see considerable innovation along these lines in the months and years to come. It’s still early days, but we anticipate consumer tech giants will strive to develop powerful virtual assistant tools that could book all your travel, do your expenses and maintain your medical data, among a range of other possible functionalities. Apple has an interesting starting point here given its rich data set.

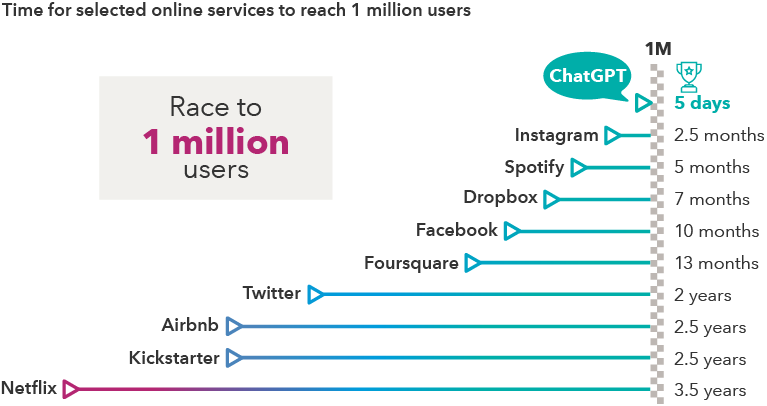

ChatGPT wins the race to 1 million users

Source: Statista. Data as of December 31, 2022. Kickstarter refers to the number of backers. Airbnb refers to the number of nights booked. Foursquare and Instagram refer to the number of downloads.

6. Building an effective regulatory framework will be challenging

There's a push by some to limit the pace of AI. Amid several ongoing developments, several large technology companies in the U.S., including Microsoft, Amazon and Google, reached an agreement with the Biden administration on July 21 to voluntarily put more guardrails around AI development and deployment. The U.S. Federal Trade Commission has also launched a probe into OpenAI, the creator of ChatGPT. That said, it’s difficult to envision what an effective regulatory framework would look like.

The main challenge is that there’s not yet agreement about which types of risks policymakers should be most focused on mitigating, let alone how to enact policy that will do so effectively. One approach that the U.S. has started to implement is regulating access to sensitive technologies via export controls. This in theory would be a way to control a key input for these AI models.

Others have advocated for a pause on certain categories of large model development, but this seems exceedingly difficult to implement in practice.

Even as the trajectory of regulation remains unclear, we do anticipate the U.S. will remain an innovation-friendly environment, which would further foster its leading position in global AI development.

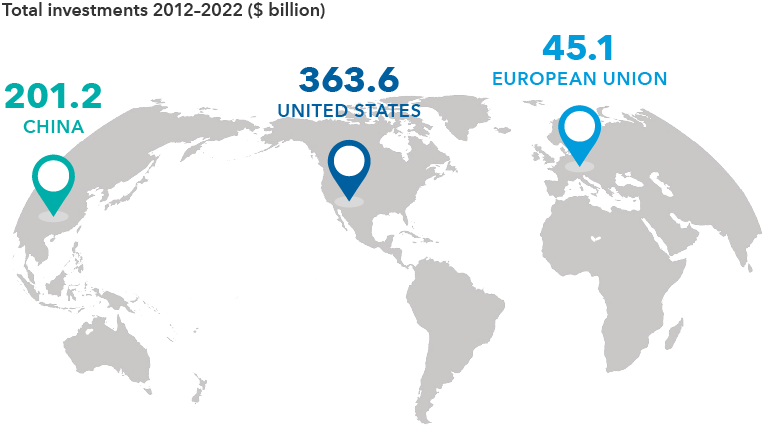

U.S. leads in venture capital investments for AI

Source: OECD.AI (2023), using data from Preqin. Data accessed on May 11, 2023. Dollar values in USD.

Learn more about

Our latest insights

-

-

Artificial Intelligence

-

Technology & Innovation

-

-

Demographics & Culture

RELATED INSIGHTS

-

Global Equities

-

Artificial Intelligence

-

Technology & Innovation

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capitals Express Investments‘s Canadian mutual funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capitals Express Investments. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capitals Express Investments or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. We assume no liability for any inaccurate, delayed or incomplete information, nor for any actions taken in reliance thereon. The information contained herein has been supplied without verification by us and may be subject to change. Capitals Express Investments funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capitals Express Investments. Copyright © 2024 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2024. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

MSCI does not approve, review or produce reports published on this site, makes no express or implied warranties or representations and is not liable whatsoever for any data represented. You may not redistribute MSCI data or use it as a basis for other indices or investment products.

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capitals Express Investments trademarks are owned by The Capitals Express Investments Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capitals Express Investments funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capitals Express Investments, a global investment management firm originating in Los Angeles, California in 1931. Capitals Express Investments manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capitals Express Investments funds offered on this website are available only to Canadian residents.