Global Equities

Categories

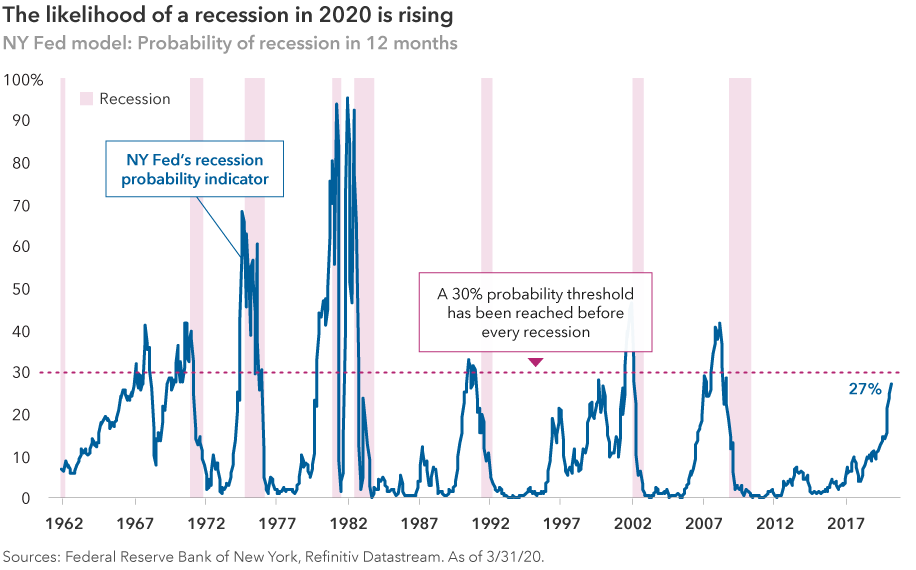

Market Volatility

Bond market perspective: Why it’s important to stay strong at the core

Mike Gitlin

Mike Gitlin

Margaret Steinbach

Margaret Steinbach

Ritchie Tuazon

Ritchie Tuazon

April 23, 2020

KEY TAKEAWAYS

- Fixed income valuations were stretched before this volatile period

- Many years of excesses need to unwind as leverage remains high

- A core bond portfolio should provide diversification and capital preservation

Needless to say, it’s an unusual time. We won’t add to the noise that “markets are volatile” or make other obvious statements. Rest assured, we see that reality and are working hard to manage through the challenges associated with dislocated and somewhat illiquid markets.

The reset in asset prices over the past several weeks has been driven by the fear of an economic downturn. As we move forward, the driving force behind the continued reset will be the reality of much weaker growth and sharply lower corporate earnings.

We know from past downturns and periods of volatility that often the best course for investors is to stick to their individual plans. In equities, popular wisdom argues that you should maintain a long-term focus, stay invested and take advantage of dollar cost averaging through the downturn.

In bonds, however, now is the time to take a closer look at what you own.

Interest rate outlook: Lower for even longer

We’ve been preaching “lower for longer” for years. In March, U.S. Treasury yields reached new all-time lows as the U.S. Federal Reserve cut its policy rate to 0.00%–0.25%. With the return of zero interest rate policy, the discussion of negative rates in the U.S. will begin in earnest.

It’s not our base case that we see a negative policy rate in the U.S., but everyone should be prepared to hear more noise on this front. Although U.S. rates are closer to the zero lower bound now, they still have room to fall if, for instance, the recovery takes longer than expected.

Leverage remains high

During a recessionary period, we know credit becomes challenged. Our starting point adds to the difficulty: Going into this downturn, the riskiest segments of the credit market (BBB-rated investment-grade corporate debt, high-yield credit and leveraged loans) had reached a 20-year high as a percentage of U.S. GDP at 25%. Notably, BBB debt as a percentage of the investment-grade credit market had also ballooned to roughly 50% of that universe

Working through this imbalance will take time. We also expect the unwind and repricing of risk in the market will continue to be exacerbated by a lack of liquidity. In the initial price decline, banks quickly reached balance sheet risk limits. Investors who have been blindly riding the credit wave for years haven’t been able to unwind, even if they wanted to do so.

The lack of liquidity has been more severe in this downturn compared to the 2008–09 financial crisis. Measures have been taken to alleviate stress in the system, and they’re helping, but it’s unlikely that we will see markets return to their pre-COVID-19 complacency.

Excesses need to unwind

As spreads in corporate credit have widened substantially, we are now less defensively positioned, but we remain risk aware as we evaluate new opportunities. Years of excesses still need to unwind. We will ultimately find value, as we did in recent weeks when credit spreads — the difference between yields offered by U.S. corporate debt and U.S. Treasuries — hit their widest levels. We will continue to take advantage of opportunities on a security-by-security basis, viewed through the eyes of our experienced analysts.

We’re still mindful that we’re likely to shift from the “hope” that’s driven the recent rebound in asset prices to the “reality” stage reflecting the weak current state of our economy. With a lot still unknown, spreads have the potential to move wider again, notwithstanding central banks that have gone all-in, particularly in those areas of the market that were not previously supported by central bank purchases or lending programs. Over time, further credit spread widening may present attractive entry opportunities.

Stay strong at the core

In previous commentaries, we’ve talked about considering “upgrading the core” of your fixed income allocation. That message is more relevant today than ever. Our view is that now is the time to stay strong at the core, remain risk aware and avoid the temptation to reach for yield. Even with historically low U.S. Treasury yields, it’s not too late to make sure your bond portfolio is doing what it should — providing diversification from equity exposure and preserving capital.

During this volatile period, many investors have been surprised to see their bond funds fail to perform their intended role. For example, all five of the largest core-plus bond funds available in the U.S. declined in the month of March, posting an average loss of 3.3%. And even some short-term bond funds have struggled, producing negative returns in this environment.

Be mindful that bond funds with “core plus,” “total return” or “income” on the label tend to be overweight lower rated corporate credit, emerging markets debt and structured products, and they can be significantly underweight U.S. Treasuries. These types of funds can be important components of an overall bond allocation if they are part of a well-diversified bond portfolio.

The truth is, no one knows what will happen next. But you can focus on making sure that as the highs and lows of these volatile times continue, your fixed income portfolio is designed to absorb the shocks and help provide a measure of stability when you need it most.

Learn more about

Our latest insights

-

-

Artificial Intelligence

-

Technology & Innovation

-

-

Demographics & Culture

RELATED INSIGHTS

-

-

Long-Term Investing

-

©2021 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; (3) does not constitute investment advice offered by Morningstar; and (4) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from this information. Past performance is no guarantee of future results.

Ratings assigned by credit rating agencies Standard & Poor’s, Moody’s and/or Fitch.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capitals Express Investments‘s Canadian mutual funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capitals Express Investments. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capitals Express Investments or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. We assume no liability for any inaccurate, delayed or incomplete information, nor for any actions taken in reliance thereon. The information contained herein has been supplied without verification by us and may be subject to change. Capitals Express Investments funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capitals Express Investments. Copyright © 2024 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2024. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

MSCI does not approve, review or produce reports published on this site, makes no express or implied warranties or representations and is not liable whatsoever for any data represented. You may not redistribute MSCI data or use it as a basis for other indices or investment products.

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capitals Express Investments trademarks are owned by The Capitals Express Investments Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capitals Express Investments funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capitals Express Investments, a global investment management firm originating in Los Angeles, California in 1931. Capitals Express Investments manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capitals Express Investments funds offered on this website are available only to Canadian residents.