Global Equities

Categories

China

China’s economy risks a sharp slowdown in growth

Stephen Green

Stephen Green

October 5, 2021

Investors in China should prepare for a rough patch. The economy is slowing, and regulations are tightening in several industries. The economic cycle turned in June/July, based on the official China Purchasing Managers Index readings and other indicators that we track. Heading into 2022, I think GDP (gross domestic product) growth will be considerably lower than the current consensus forecast of around 5%.

Here are a few reasons that lead me to this view:

1. Credit is tight in the real estate market.

Primary real estate sales are about 15% of GDP, and the indirect demand the sector generates makes it even more important to the economy. And credit is tightening in the real estate sector. Home-buying restrictions could be loosened. But, with low inventories and contracting housing supply, any loosening could result in even higher house prices, undermining the government’s key policy objective that “housing is not for speculation.”

Evergrande, the country’s second-largest developer, is likely headed for a managed bankruptcy process. The unwinding will likely involve selling off Evergrande assets project by project to SOEs (state-owned enterprises).

The government’s top priority is to protect those who pre-bought Evergrande apartments, which reportedly amounts to approximately 600,000 buyers. Suppliers to Evergrande are already being “paid” in the form of property that’s been cut in price by 20% to 30%, based on what my colleagues and I have heard from our sources.

But Evergrande is just the most obvious entity in a troubled sector. Dozens of medium-sized developers have weak cash flows and are having trouble obtaining bank loans or issuing debt. Some are slashing prices in order to raise cash. In the past, the larger developers would come in and buy the unfinished projects, but that’s unlikely now.

There’s also the likelihood of a property tax program that will be piloted in some cities. Many middle-class urban households own two properties, and this could dampen consumer demand, depending on the tax rate that may be set and its scope.

China’s economy appears to be weakening

Source: FactSet. Latest available data as of September 30, 2021. An index reading of 50 signals no change since the previous month. Above 50 signals an increase (or improvement), below 50 a decrease (or deterioration). The greater the divergence from 50, the greater the rate of change signaled.

2. Consumer confidence is ebbing, and retail sales growth is slowing.

Consumer confidence never fully recovered after China’s initial COVID-19 outbreak in early 2020. And neither did income growth, particularly for lower income groups. Retail sales growth is still positive, but again, the pace of growth is declining. Car sales are also falling in absolute terms though that’s mostly due to supply disruptions due to a lack of components, according to our analysts who cover the sector. Youth employment in urban areas is pushing up, while overall surveyed employment still has not returned to its pre-COVID-19 base.

The government’s Common Prosperity agenda on improving life for the lower middle class could also result in a spate of taxes on property, inheritance, luxury and alcohol, which would impact a wide swath of the upper middle class, potentially further dampening consumer sentiment.

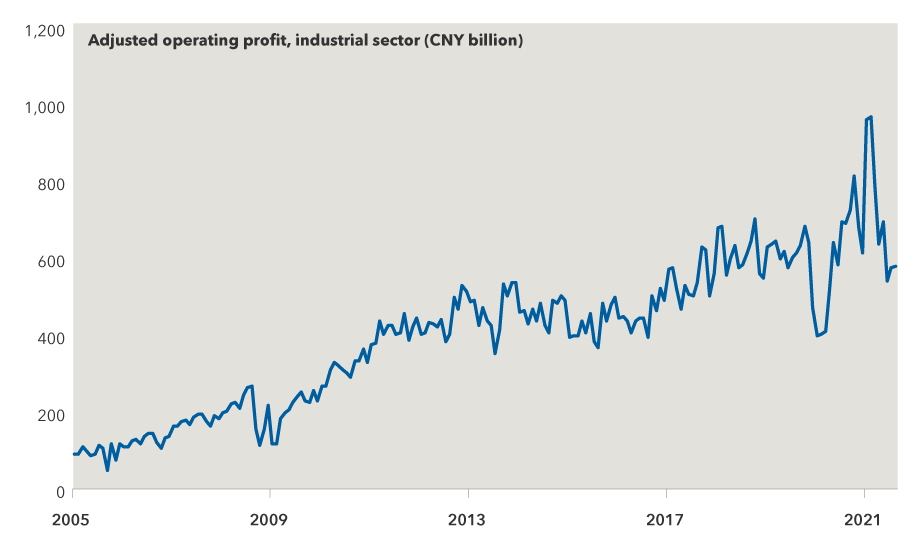

3. Heavy industry could see excess capacity, and industrial profits have softened.

The real estate boom of 2018-20 supported high levels of demand for steel. That, plus supply reforms that wiped out old and excess capacity in the mid-2010s, meant that heavy industry returned to health. With end demand contracting now, we could see some excess capacity return. The data is volatile, but the trendline shows that industrial profits are now below pre-COVID levels, which could dampen corporate capital investment in 2022.

Profit in China's industrial sector has slowed

Source: Capital Strategy Research. Data as of August 1, 2021

Government has tools at its disposal to stimulate

No doubt, the government has tools at its disposal to stimulate the economy. China’s benchmark interest rate is 4%, which is very high compared to other economies, so the People’s Bank of China has room to lower rates. We could even see a 25 to 50 basis points cut in interest rates in the next few months.

The challenge authorities face is that, at a time when they want to continue to clamp down on housing and local government debt, cutting rates may be risky. Beijing also might worry about lowering rates when the rest of the world is hiking, potentially dampening capital inflows. So, while rate cuts might suggest significant loosening, I doubt they’ll be enough.

When Beijing has stimulated growth in previous cycles, it has usually both cut rates and told the banks to lend more, which creates end demand by stimulating the property and infrastructure sectors. But while property is paid for by households, infrastructure is paid for by local government-owned entities so it’s a de facto government liability.

This time, there’s much less room on the fiscal front with government debt, when properly measured, at more than 100% of GDP and rising rapidly. Beijing has tried to make this debt more transparent by funding more of it through public bonds, but it has not effectively curbed the still-large “hidden debt.”

I also believe that, in the near-term, Beijing is comfortable with sacrificing growth to achieve key strategic priorities.

While many are focused on the 20th Central Communist Party (CCP) Congress in fall 2022 as a reason to expect a stimulus package, I think the leadership now has its eyes on 2035-40, when they envision being a strong and technologically advanced country. I believe the government is willing to take short-term pain for long-term gain.

CCP General Secretary Xi Jinping, in addition to wanting to deflate the property market, wants funding to flow to the regime’s strategic priorities environmental protection, electric vehicles, semiconductors and weapons. It’s clear as well that the CCP today wants a different relationship with the private sector than the party of yesterday.

As a result, I do not expect any significant loosening of policy in the next three to six months.

I could be wrong, of course. For sure, there will be a lot of pressure to loosen by year-end, especially if fourth-quarter economic data is well below expectations. If that’s the case, we will probably get some rate cuts and perhaps a turn to proactive fiscal policy in 2022.

But my base case is that these will not be big enough to turn growth around until at least the second half of 2022 and maybe later. Given that consensus market expectations are for an official GDP growth rate of 5% for 2022, I think there is a significant risk of a negative surprise.

Learn more about

Our latest insights

-

-

Artificial Intelligence

-

Technology & Innovation

-

-

Demographics & Culture

RELATED INSIGHTS

-

-

Technology & Innovation

-

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capitals Express Investments‘s Canadian mutual funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capitals Express Investments. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capitals Express Investments or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. We assume no liability for any inaccurate, delayed or incomplete information, nor for any actions taken in reliance thereon. The information contained herein has been supplied without verification by us and may be subject to change. Capitals Express Investments funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capitals Express Investments. Copyright © 2024 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2024. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

MSCI does not approve, review or produce reports published on this site, makes no express or implied warranties or representations and is not liable whatsoever for any data represented. You may not redistribute MSCI data or use it as a basis for other indices or investment products.

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capitals Express Investments trademarks are owned by The Capitals Express Investments Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capitals Express Investments funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capitals Express Investments, a global investment management firm originating in Los Angeles, California in 1931. Capitals Express Investments manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capitals Express Investments funds offered on this website are available only to Canadian residents.