Global Equities

Categories

Emerging Markets

Friendshoring brings industrial-sized investment opportunity

Jeff Garcia

Jeff Garcia

Brad Freer

Brad Freer

Lisa Thompson

Lisa Thompson

February 29, 2024

Investors may be surprised to learn that the latest flashpoint for electric vehicle manufacturing is nowhere near the high-tech hubs of Silicon Valley or Shenzhen. It’s a town in northern Mexico called Santa Catarina, near Monterrey.

That’s where Tesla has announced it will build its first EV manufacturing plant in Mexico, a so-called gigafactory that is expected to cost US$5 billion and will reportedly break ground next week, according to local development officials in the state of Nuevo León.

The factory is a huge win for Mexico’s fast-growing economy, but it’s just the latest in a string of global trade victories that have catapulted Mexico ahead of China and Canada as the No. 1 trade partner of the United States. In 2023, for the first time in decades, the U.S. purchased more goods from Mexico than anywhere else in the world.

Mexico rises to the top on a wave of friendshoring

Sources: Capitals Express Investments, U.S. Census Bureau. Includes both imports and exports. Figures are seasonally adjusted. As of December 2023.

A friend in need is a friend indeed

“Mexico has benefited probably more than any other country from the trend of friendshoring,” says Capitals Express Investments analyst Jeff Garcia, who covers Latin America.

Friendshoring, a derivative of the term offshoring, is a deliberate policy decision to encourage trade with friendly neighbours at a time when geopolitical tensions are increasing around the world, Garcia explains. It’s not a new concept, but it was accelerated by the COVID-19 pandemic as traditional supply chains broke down and companies were forced to find alternatives. Over the past few years, the redrawing of supply chains has been a major boon to India, Vietnam, Thailand, Indonesia and especially Mexico, given its proximity to the world’s largest economy.

“This is a watershed moment for Mexico,” Garcia adds. ”China was the United States’ No. 1 trade partner for about a decade. Before that, it was Canada. So it’s a big change. There’s a saying in Mexico that goes, ‘Tan lejos de Dios y tan cerca a los Estados Unidos,’ which translates to, ‘So far from God, but so close to the United States.’ And it basically means that being on good terms with the world’s largest economy is good for Mexico. And it’s good for the U.S., as well.”

In the years ahead, Garcia expects Mexico’s position to continue improving given the advantages it offers to companies that want to tap into the U.S. market. Those advantages include a skilled labour force at an attractive cost, solid infrastructure in the north, and easy access to relatively inexpensive U.S. oil and natural gas.

In fact, not long after Tesla announced its decision to build a new EV factory in Mexico, one of its top competitors, China-based BYD, said it was planning to follow suit — singling out the same industrial area in Nuevo León. Northern Mexico has long been a popular location for automotive assembly. Ford, General Motors, BMW, Daimler, Toyota and Honda all have plants there. More than 75% of the cars assembled in Mexico are exported to the U.S., according to the Mexican Automotive Manufacturers Association.

U.S.-Mexico trade features a growing and diverse line of products

Sources: Capitals Express Investments, World Bank Integrated Trade Solution (WITS). Labels represent products that rank among the top 20 product categories by export value as of 2022. Latest figures available as of February 2024.

Mexico’s industrial renaissance is in full swing

In addition to friendshoring, the investment theme most prevalent in Mexico is the “industrial renaissance,” or reawakening of large-scale industrial spending after decades of underinvestment. The trend bodes well for companies in the construction industry, heating and air conditioning, transportation and related businesses.

“This is an exciting turning point for emerging markets such as Mexico and India, because it represents a broadening of opportunities,” says equity portfolio manager Brad Freer. “It’s not just China anymore, it’s China plus one.”

“China plus one” refers to the strategy being followed by many multinational companies seeking to diversify their supply chains. They aren’t abandoning China, Freer explains, they are adding capabilities elsewhere. Moreover, Chinese companies are among the biggest participants in this strategy, with the same motivations as U.S. and European companies. The days when the world could rely on one source of cheap manufacturing are over. Diversified supply chains are no longer a luxury but a requirement.

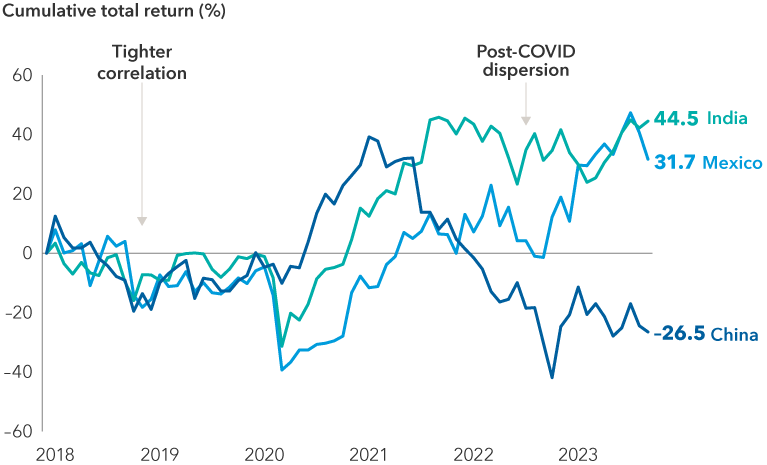

Returns among large EMs have diverged post-COVID

Sources: MSCI, RIMES. Returns reflect MSCI India Index, MSCI Mexico Index, and MSCI China Index. Five-year time period shown to reflect returns pre and post-COVID. Data as of September 30, 2023.

On a recent research trip to Monterrey and Tijuana, Freer and Garcia visited several real estate companies, construction firms and auto manufacturers. They also spent half a day touring the Mexican facilities of Carrier Global, one of the world’s largest heating, ventilation and air-conditioning (HVAC) companies.

“I was shocked to see the magnitude of what’s happening,” Freer says. “It reminded me of the cities I visited in China during the 1990s and early 2000s, with these bustling multi-million square foot facilities and thousands of workers building at scale. That's now happening in northern Mexico at a rate that I think is surprising to a lot of people.”

Economic and market tailwinds

The changes are clearly visible in Mexico’s economy, which has been growing at a rapid pace in recent years, providing a healthy tailwind for all types of companies doing business there. The MSCI Mexico Index rose more than 40% in 2023, besting the S&P 500 Index of U.S. stocks by a full 14 percentage points.

Historically speaking, Mexico’s economy has tended to grow roughly in line with the U.S. economy, translating into a modest average 1% to 2% growth in GDP per year over the past two decades.

“What's interesting is that during the last few years, Mexico’s economy has grown by two or three times that rate,” Garcia notes. “Part of the reason is COVID recovery, of course. But another important catalyst has been the increasing level of trade with the U.S, and the modernization of free-trade agreements between the U.S., Mexico and Canada. That's been a big reason why Mexico's GDP is growing well ahead of its long-term trend.”

Mexico’s economic growth has surged in recent years

Sources: Capitals Express Investments, The World Bank. Latest figures available as of February 2024.

Amid this remarkable success, Mexico still faces challenges. For example, the benefits of rapid economic development in the north have not been shared by Mexico’s southern regions, where incomes are far lower and job opportunities are scarce. Similarly, cities near the U.S. border tend to have excellent infrastructure, while modern highways are less prevalent in the south.

“Mexico is going through significant change right now, and it is benefiting greatly from the reimagining of supply chains around the world,” says equity portfolio manager Lisa Thompson.

“However, when you go a little bit further away from the border, it’s clear that Mexico isn’t having the same type of success attracting foreign investment,” Thompson says. “There are some big infrastructure weaknesses. They have not invested enough in the electricity grid. And that is holding back advancement in other parts of the country.

“This is an opportunity for Mexico to seize,” she adds. “But, as always, it’s about the execution. I think it will be an exciting story to watch in the years ahead.”

Learn more about

The MSCI Mexico Index is a market capitalization-weighted index designed to measure the results of 24 large- and mid-cap companies in Mexico.

S&P 500 Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks. The index is unmanaged and, therefore, has no expenses. Investors cannot invest directly in an index.

Our latest insights

-

-

Artificial Intelligence

-

Technology & Innovation

-

-

Demographics & Culture

RELATED INSIGHTS

-

-

Technology & Innovation

-

Emerging Markets

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capitals Express Investments‘s Canadian mutual funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capitals Express Investments. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capitals Express Investments or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. We assume no liability for any inaccurate, delayed or incomplete information, nor for any actions taken in reliance thereon. The information contained herein has been supplied without verification by us and may be subject to change. Capitals Express Investments funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capitals Express Investments. Copyright © 2024 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2024. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

MSCI does not approve, review or produce reports published on this site, makes no express or implied warranties or representations and is not liable whatsoever for any data represented. You may not redistribute MSCI data or use it as a basis for other indices or investment products.

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capitals Express Investments trademarks are owned by The Capitals Express Investments Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capitals Express Investments funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capitals Express Investments, a global investment management firm originating in Los Angeles, California in 1931. Capitals Express Investments manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capitals Express Investments funds offered on this website are available only to Canadian residents.