Global Equities

Categories

Japan

Japan: Will reforms unlock stock valuations?

Eu-Gene Cheah

Eu-Gene Cheah

Akira Horiguchi

Akira Horiguchi

Dickon Corrado

Dickon Corrado

Emily Liao

Emily Liao

September 5, 2023

A significant shift is underway in Japan, and equity markets are taking notice. It may not have been obvious to U.S. dollar-based investors, but in local currency terms, Japanese equities as measured by the MSCI Japan Index have climbed 25% year to date (as of August 31, 2023).

The wave of optimism has been driven by two key factors: inflation and reforms. While inflation has been challenging for many developed economies, it’s a welcome sign in Japan, which has been battling deflation for three decades. Sustained and healthy inflation could change the mindset in Japan from saving to investing.

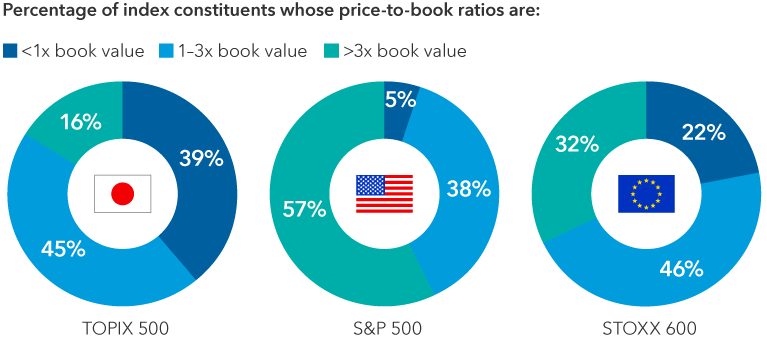

In terms of reforms, there is tremendous emphasis on improving corporate governance, and companies are focusing more on shareholder returns. In a recent move, the Tokyo Stock Exchange asked all listed companies to enact policies to improve profitability, long-term returns and valuations. About 39% of companies in the TOPIX (an index comprising Japanese stocks) trade below book value, compared to just 5% for companies in the S&P 500 Index.

Book values are depressed in Japan

Sources: Capitals Express Investments, FactSet, Refinitiv Datastream, Standard & Poor’s, STOXX, TOPIX. The price-to-book ratio is the ratio of a company's publicly traded share price to its equity value per share. As of August 18, 2023.

Many Japanese companies have also fallen behind on converting information into digital formats and are now making concerted efforts to catch up, which could boost productivity. Put together, these steps can create a virtuous circle with a potentially positive impact on corporate earnings and valuations.

The economic transformation is not entirely new. It began around 10 years ago with Abenomics — then-Prime Minister Shinzo Abe’s program aimed at reinvigorating Japan’s stagnant economy through a combination of monetary policy, government spending and structural reforms. But investor optimism has fluctuated. That said, in our recent travels through Japan, where we and many Capitals Express Investments portfolio managers and analysts met with various policymakers and corporate managements across many industries, we observed that the desire for change is more palpable today than it has been in the prior two decades.

Some other factors that support our positive outlook: valuations appear reasonable compared to other markets, the political situation is relatively stable, foreign investment in manufacturing is coming back and tourism has rebounded since COVID-19 restrictions were lifted. Interest rates also remain low relative to other developed markets.

Against this backdrop, we have additional views on Japan and areas of the market that may present potential investment opportunities.

1. Japanese companies occupy niches in key industries

For all its economic woes, Japan has created a tremendous competitive advantage in certain industries. Japanese firms have developed unique technologies in niche markets from which they’ve been able to build durable businesses with highly defensible moats. These include areas like industrial automation equipment, sensors, inspection tools for semiconductor manufacturing, energy-efficient air conditioning systems and battery technology. Medical devices and pharmaceuticals are other areas where Japanese companies have built market share.

These types of companies should have long product cycles as we see an industrial renaissance in developed economies and ongoing industrialization in emerging markets.

SMC, for instance, is a leader in specialized components for automation equipment and semiconductor production. Shin-Etsu is the world’s largest maker of silicon wafers for semiconductor products, while TDK is one of the largest manufacturers of high-end batteries and specialized circuits used in electric vehicles.

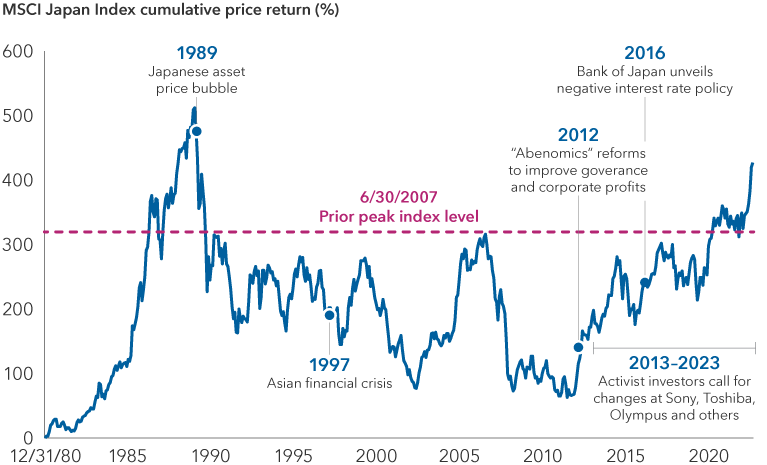

Japanese stocks trade at highest levels since early 1990

Sources: Capitals Express Investments, MSCI, RIMES. Cumulative price returns shown from December 31, 1980, to July 31, 2023. Returns shown in Japanese yen. The cumulative return is the total change in the investment price over a set time. As of July 31, 2023. Past results are not predictive of results in future periods.

2. Corporate reforms are gaining traction

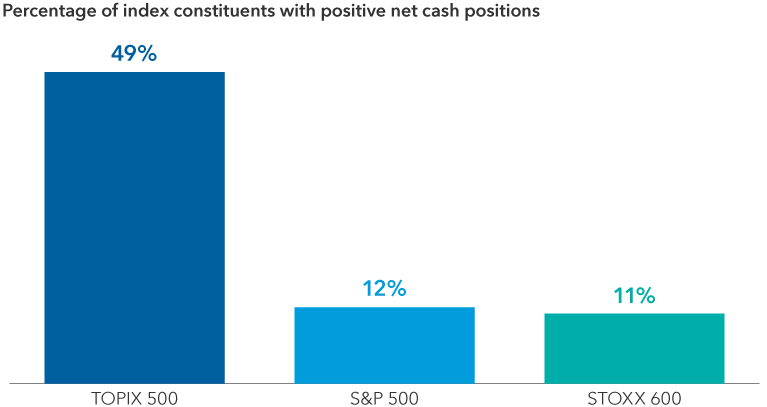

Many Japanese companies have excelled in cutting-edge areas of science and engineering. However, equity prices in most cases have been hurt by subpar corporate governance. A number of companies have hoarded cash, created insular corporate structures, and operated conglomerates (large and small) that have not always been efficient or profitable.

Since the start of Abenomics in 2012, corporate Japan has been on a journey to improve profitability, capital allocation and corporate governance. But while progress has been painfully slow, in part due to Japan’s cautious approach to change, there is a stronger sense of urgency to address cash-heavy balance sheets and inefficient business lines.

We now believe there is greater alignment between companies and the government to improve governance standards, business models and capital structures. Over the next few years, this may well result in improved shareholder returns through divestitures, higher dividend payouts and share buybacks.

In our meetings with officials from the Ministry of Economy, Trade and Industry and the Financial Services Agency, they highlighted how company book values were much lower than those in the U.S. and Europe, and that this needed to be fixed. They also voiced support for more acquisitions between domestic companies.

Japan Inc. is cash heavy

Sources: Capitals Express Investments, FactSet, Refinitiv Datastream, Standard & Poor's (U.S.), STOXX (Europe), TOPIX (Japan). Net cash reflects the difference between the cash and short-term securities reported on a company's balance sheet and its outstanding debt. As of August 18, 2023.

3. Potential for M&A and consolidation to add value

More specifically, the government’s recent proposal addressing governance standards for mergers and acquisitions would make it more difficult for boards to reject reasonable takeover offers without justification.

This would represent monumental change. We believe merger-and-acquisitions activity has the potential to unlock the biggest hidden value remaining in Japan, which is the mountain of cash doing nothing across a multitude of corporate balance sheets.

At the height of their influence and power in the late 1980s, many Japanese companies decried the ruthless takeover environment in the United States. They placed more emphasis on operating large and stable businesses. Japan favoured lifetime employment, seniority-based compensation and shared salary cuts over job cuts.

In sum, we don’t expect changes to happen overnight. They will likely be gradual, but getting ahead of those opportunities as investors is important.

4. Transforming legacy businesses may unlock shareholder value

Some companies have been reinventing themselves by shedding noncore businesses and narrowing their business focus. In others, there is new leadership driving change or existing managements and boards that seem willing to make changes.

Here are several examples:

- Pharmaceuticals firm Daiichi-Sankyo was once hampered by poor product development, a portfolio of undifferentiated drugs and the unsuccessful acquisition of India’s largest generic drugmaker. Daiichi shifted course several years ago, cutting many of its R&D programs to focus on building what has become a promising pipeline of novel cancer treatments. It now ranks as one of Japan’s most valuable companies by market capitalization, boasts a differentiated antibody drug conjugate (ADC) platform and a blockbuster drug used to treat breast cancer.

- Toppan is looking to address its cash-heavy balance sheet. Its new president has been deemphasizing the company’s commercial printing business in favour of specialty packaging. Toppan has launched a large share buyback program, shrunk the size of its board and introduced a target for return on invested capital. It also sold equity stakes in two of its businesses.

- Industrial conglomerate Hitachi has been shrinking its portfolio, divesting interests in its construction machinery, metals and auto parts businesses. The company aims to pay out approximately 50% of its net income in dividends and share buybacks.

Broadly speaking, we think these kinds of self-help stories can help support long-term growth.

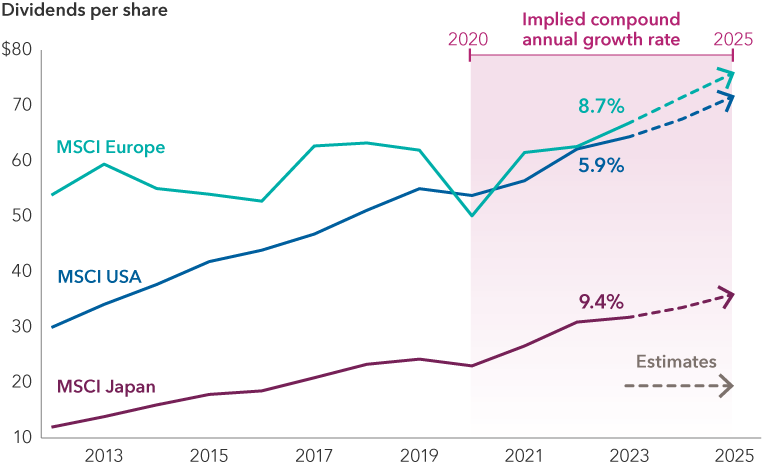

Dividend growth in Japan looks encouraging

Source: FactSet. Dividends reflect the aggregate amount paid by companies on a per-share basis in the respective indices. Data for 2023–2025 is based on consensus estimates as of May 31, 2023. Compound annual growth rate is the mean growth rate of an investment over a specified period of time longer than one year.

5. Spending on enterprise software should grow amid digital transformation

Japan is playing catch-up when it comes to moving into the digital age. The pandemic exposed this weakness when the government struggled to distribute emergency payments and as workers were challenged to work remotely.

Many Japanese companies need to upgrade their legacy computer systems, which we believe foreshadows a rise in information technology investment. Given the country’s aging demographics and persistent labour shortage concerns, businesses will need to improve productivity and increase automation. OBIC is one company that has benefited from this trend; it has seen sales for its computer cloud software grow for the past several years.

Meanwhile, Nomura Research Institute (NRI) is an example of how big companies are seeking to harness the productivity benefits of artificial intelligence (AI), which NRI is using to help large enterprises organize their proprietary data in a format that can train very large datasets for AI.

6. Geopolitical tensions are reviving manufacturing investments

Japan is a country with relative social stability, and as an export-driven economy, it has a proven and reliable manufacturing base. With growing risks to doing business in China, Japan has been attracting more foreign investment. Manufacturing costs are also more reasonable after decades of deflation and the weaker yen.

One case worth watching is the construction of Taiwan Semiconductor’s plant in Kumamoto, where it reportedly may build a second facility as well. Japan’s government has brought in more than USS14 billion in planned investment since 2021 from companies in the U.S., Europe, South Korea and Taiwan. Among those are South Korea-based Samsung Electronics and U.S.-based Micron Technology, both leaders in the development of memory chips.

We think Japan is in a position to capture some higher-end manufacturing as multinationals seek to diversify their supply chains in Asia. Countries like Vietnam and Cambodia can make items like sneakers and toys but lack the necessary expertise and infrastructure for more technologically sophisticated products. If this trend continues, it would be a sharp reversal from the past and could potentially reinflate the economy and provide a boost to regional business hubs.

7. A rebound in the yen should be additive to stock returns

A weakening yen has eroded Japanese stock returns for U.S. dollar-based investors. The Japanese currency weakened from 103 yen to the dollar at the end of 2020 to the current level above 145 yen to the dollar. The Bank of Japan’s (BOJ’s) bond-buying policy of depressing yields, known as yield curve control, combined with an anemic economy, have weighed on the currency.

Over the last couple of months, the BOJ has acknowledged that inflationary pressures have risen and adjusted monetary policy to allow 10-year yields to rise to 1.0%.

In the view of our Japan economist Anne Vandenabeele, it’s likely that inflation will persist above the BOJ’s target of 2% over the next 12 to 18 months. The central bank could therefore be in a position to end its negative interest rate policy next year and further loosen its controversial yield curve control policy as well (although the BOJ will likely continue to buy bonds to manage the rise in yields). This chain of events is expected to lead to the yen plateauing at these levels, or even strengthening from here, although much will also depend on other central banks and U.S. rates, in particular.

And a stronger yen should benefit U.S. dollar-based investors purely from the currency translation effect on portfolios.

From a fundamental perspective, many of Japan’s major exporters such as the auto companies, have diversified their manufacturing bases with factories around the world. As such, the impact of a strengthening currency on corporate earnings should be much more muted than in the past.

8. Loss of reform momentum and a global downturn are risks

We’ve seen similar market rallies fizzle over the past decade. The introduction of Abenomics and subsequent corporate reforms in 2014 and 2015, along with the growing presence of U.S. activist hedge funds in Japan, have led to bursts of exuberance.

While positive developments are taking shape, we are taking a measured approach. Foreign investors make up a large portion of Japan’s equity market. The country’s economy is export-driven and heavily focused on industrial production. If the global economy weakens or reforms lose steam, stocks could come under pressure in a risk-off environment.

Nevertheless, we are currently more positive on Japan than we have been over the past two decades. The number of portfolio managers and analysts who have visited Japanese companies continues to grow, and the discussion on where the opportunities are is robust across equity groups and portfolios.

Learn more about

Eu-Gene Cheah and Akira Horiguchi are portfolio managers for Capitals Express Investments International Equity Fund (Canada).

The book value of a stock is theoretically the amount of money that would be paid to shareholders if the company was liquidated and paid off all of its liabilities.

The MSCI Europe Index captures large-and mid-cap representation across 15 developed market countries in Europe. With 424 constituents, the index covers approximately 85% of the free float-adjusted market capitalization across the European developed markets equity universe.

The MSCI Japan Index is designed to measure the performance of the large-and mid-cap segments of the Japanese market. With 237 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in Japan.

The MSCI USA Index is designed to measure the performance of the large-and mid-cap segments of the US market. With 627 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in the US.

S&P 500 Index is a market-capitalization-weighted index based on the results of 500 widely held common stocks.

The STOXX 600 Index represents large-, mid- and small-capitalization companies across 17 countries of the European region: Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Norway, Poland, Portugal, Spain, Sweden, Switzerland and the United Kingdom.

The TOPIX 500 Index is a capitalization-weighted index designed to measure the performance of the 500 most liquid stocks with the largest market capitalization that are members of the TOPIX Index.

Our latest insights

-

-

Artificial Intelligence

-

Technology & Innovation

-

-

Demographics & Culture

RELATED INSIGHTS

-

Global Equities

-

Artificial Intelligence

-

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capitals Express Investments‘s Canadian mutual funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capitals Express Investments. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capitals Express Investments or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. We assume no liability for any inaccurate, delayed or incomplete information, nor for any actions taken in reliance thereon. The information contained herein has been supplied without verification by us and may be subject to change. Capitals Express Investments funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capitals Express Investments. Copyright © 2024 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2024. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

MSCI does not approve, review or produce reports published on this site, makes no express or implied warranties or representations and is not liable whatsoever for any data represented. You may not redistribute MSCI data or use it as a basis for other indices or investment products.

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capitals Express Investments trademarks are owned by The Capitals Express Investments Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capitals Express Investments funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capitals Express Investments, a global investment management firm originating in Los Angeles, California in 1931. Capitals Express Investments manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capitals Express Investments funds offered on this website are available only to Canadian residents.