Global Equities

Categories

Market Volatility

Capitals Express Investments CEO Tim Armour on weathering the coronavirus

Tim Armour

Tim Armour

March 11, 2020

KEY TAKEAWAYS

- News of the continued spread of coronavirus — and the recent plunge in oil prices — has sent stocks plummeting toward bear market territory, and bond yields have reached unprecedented lows.

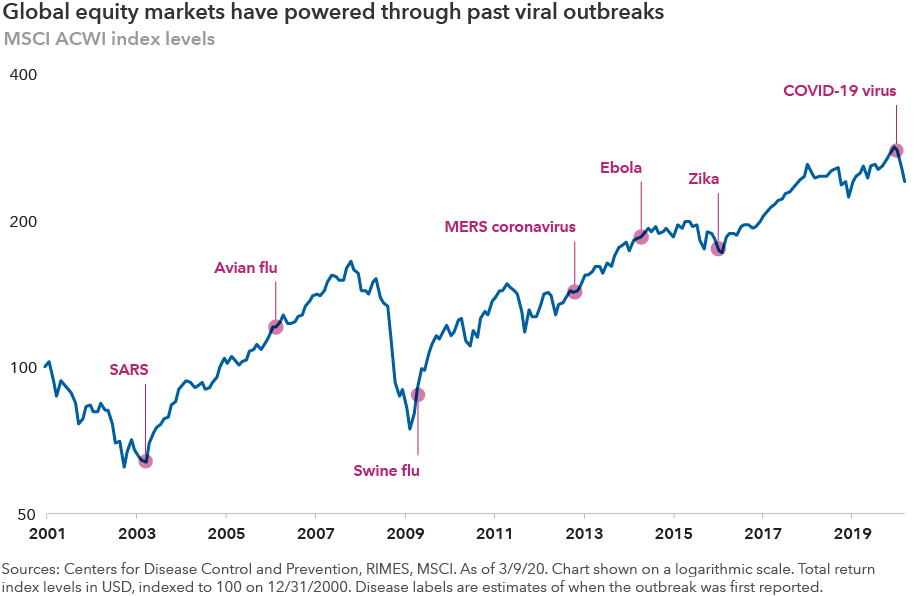

- While the virus represents a new challenge, there is nothing new about market volatility. Markets have survived viral outbreaks in the past.

- Investors who can look past the current environment and stay the course can benefit over the long run.

Rising fears over the continued spread of the coronavirus have led to a sharp stock market decline as investors grapple with its impact on the global economy. On Monday, March 9, in reaction to news of the virus spread and the recent oil shock, Standard & Poor’s 500 Composite Index fell 7.6%, triggering a 15-minute trading halt. In this interview, Capitals Express Investments Chairman and CEO Tim Armour offers his perspective on the latest events and what Capital is doing in portfolios to help guard against market volatility.

1) What is your sense of the coronavirus (COVID-19) outbreak and market reaction?

Until January 2020, most of us had never heard of this virus. In short order, we have grown increasingly concerned about the prospect of a global pandemic and its impact on the global economy. People are understandably frightened because this is a new disease, and there is much uncertainty over how it will all play out. First and foremost, the virus has a real human cost. We don’t know how many people are going to get ill or, worse yet, how many may die. Of course, our first thoughts are with the people who have fallen ill and their families.

While this disease is new, there have been many pandemics and other crises in the past, and markets have survived them all. Today, a fair amount of panic has taken hold around the world, and I expect in the coming weeks that a rising number of cases may alarm many people. As an organization, we have been studying the history of pandemics and the pattern they have tended to follow. There have tended to be hot spots and flare-ups, and they lasted for a while, but then they went away. Eventually, the spread of the virus will slow down and people will get back to normalcy, as will markets.

2) What does this mean for the U.S. economy?

We are already seeing signs of a slowdown in the U.S., not only on the supply side as businesses brace for the road ahead, but also on the demand side. By now we have all heard of large conferences and entertainment events being canceled, firms postponing large meetings, and consumers delaying vacations and seeking to reduce their social contact.

That means businesses related to travel, leisure, entertainment and recreation are likely to be the most impacted, not to mention oil and other commodities where we have already seen a collapse in global demand. A U.S. recession has become increasingly likely. We could see corporate earnings turn negative in the first quarter, which would continue to dampen investor sentiment.

On the positive side, the U.S. economy remains among the most resilient in the world. It has a history of bouncing back from adversity. Interest rates are low, and the decline in oil prices should further support the consumer. What’s more, in China the spread of the virus appears to have peaked. Given that, I think the peak of its spread globally will occur sooner than many people anticipate.

3) What does it mean for markets?

We are experiencing a market decline that we have not seen since the Global Financial Crisis. As I speak today, March 9 is the 11th anniversary of the market bottom during the Global Financial Crisis — and the market noted the anniversary by recording the largest single-day point decline we have ever seen.

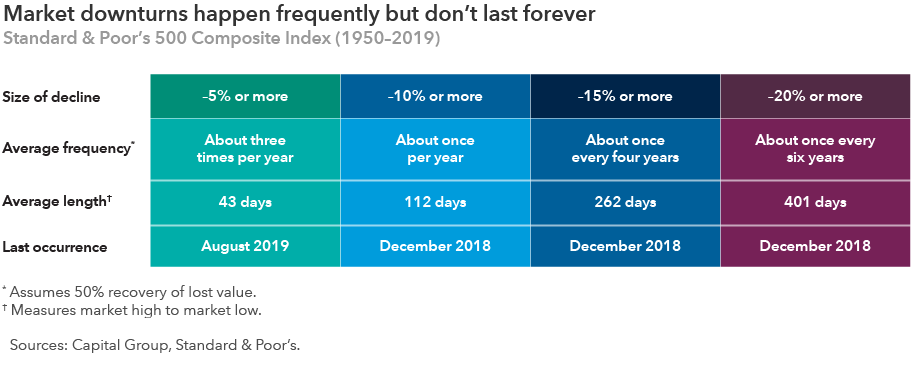

As of the market close on Monday, the broader equity markets, as measured by the S&P 500, were down nearly 19% from their peak earlier in the year, and we may soon be in bear market territory, which is defined by a decline of more than 20%. This would be the first bear market after more than a decade of generally strong market returns. As a result, in general, equities appeared to be fully valued by most measures heading into this recent period, and markets could remain volatile for some time. In addition to the uncertainty resulting from the spread of the virus, the U.S. is in an election year.

Turning to the bond market, we have seen a flight to safety that has pushed bond yields to unprecedented lows. The yield on the 10-year U.S. Treasury fell to 0.5%. Interest rates could go still lower as the U.S. Federal Reserve seeks to provide liquidity to markets through interest rate cuts and quantitative easing. Over time, low interest rates provide support to equities.

While the pace and magnitude of the recent volatility can be unsettling, it is not entirely surprising. Investor sentiment is fragile and will likely remain so until the spread of the virus slows. In times like these, resilient investors who can demonstrate patience can be rewarded over the long term.

I take some comfort in seeing that the Federal Reserve has demonstrated its willingness to take aggressive action, cutting interest rates 50 basis points in an emergency meeting on March 3, which lowered its target range to between 1.00% and 1.25%. The Fed stated that it is "closely monitoring developments and their implications for the economic outlook, and will use its tools and act as appropriate to support the economy." Markets are generally expecting an additional cut at the Fed’s next scheduled meeting, to be held on March 17 and 18.

4) How does this compare with crises in the past?

In the 37 years I have spent as a professional investor at Capital, I have experienced a number of unsettled markets, including the U.S. savings and loan crisis in the late 1980s, the tech and telecom bubble that ended in March 2000, and the Global Financial Crisis of 2008 and 2009. Each of these crises was very different, with very different underlying conditions. But in each case, the markets bounced back. I believe the markets, and great companies, will survive the current market decline and rebound.

Let me share with you the words of two of my predecessors who mentored me through periods like this. Jim Fullerton, as Chairman of Capital in 1974 in the depths of one of the worst bear markets we have ever seen, wrote these words that are relevant today:

“One significant reason why there is such an extreme degree of bearishness, pessimism, bewildering confusion and sheer terror in the minds of brokers and investors alike right now is that most people today have nothing in their own experience that they can relate to, which is similar to this market decline. My message to you, therefore, is courage! We have been here before. Bear markets have lasted this long before. Well-managed mutual funds have gone down this much before. And shareholders in those funds and the industry survived and prospered.”

And Jim Rothenberg, former Chairman of Capitals Express Investments, said this amid the Global Financial Crisis in 2008:

“I have seen many turbulent markets and know how hard it is to avoid getting caught up in the here and now. This is especially true when the media bombards us hourly with news, speculation and rumour. I also know, though, that as long-term investors we must focus on the real world underneath the noise and mesmerizing flow of data.”

5) Should investors expect a quick recovery?

At this point, I do not think it is realistic to expect a quick recovery. Circumstances may very well get worse before they get better. But I believe eventually markets will rebound. This too shall pass. When it does, long-term investors who can tune out the daily white noise — and red numbers flashing across their screens — and focus on the long term should ultimately be rewarded.

I take the view that we will deal with outbreaks like COVID-19 and eventually we will adjust to it. At Capital, we are taking every precaution to prepare for it. We expect that we will be dealing with the COVID-19 virus for some time, possibly a year or two.

One further point: We have offices in Singapore, Beijing, Hong Kong and Tokyo with a significant number of associates. They have already lived through four weeks of COVID-19. In China, people are already starting to go back to work. If you look at our associates in these offices, they were dealing with an emergency a month ago and today they are returning to a less disruptive life and business environment. They feel things are much more under control. I look at that as a pattern we are likely to experience here in the U.S. and Europe at some point.

6) What are you doing in your portfolios now to guard against market volatility?

Our company was founded in 1931 in the depths of the depression, with the aim of managing investment mandates designed to do well in volatile market periods. We seek to protect our investors’ capital on the downside, and we invest for the long run. This is true for Capitals Express Investments globally as it is for our investors in Canada, where we have offered portfolios since 2002. I recently looked at our funds’ results during this admittedly brief period of turmoil. Looking at our Canadian funds, you will find that many of our funds have done what we aspire for them to do: They have held up relatively better than their primary benchmarks (as of March 9, 2020).

7) What is Capitals Express Investments doing to ensure continuity as we take care of client assets?

Obviously our first concern is to ensure the health and safety of our associates. We hope the same for investors and advisors. But rest assured as this situation evolves, our more than 350 investment professionals in offices around the world continue to do what they have always done: analyzing companies and making real-time judgements about their potential long-term value. In-depth, fundamental research and a long-term view of markets is at the core of what we do. We will do our very best to provide investors with a smooth and less volatile experience than the broader markets.

8) What should investors be doing?

In periods of declining markets, emotions run high, and that’s natural and understandable. But it is exactly in times like this that a long-term orientation is important. Based on my prior experiences and what has historically occurred, I firmly believe markets will rebound and life will return to normal. Now more than ever, investors should be in close communication with their advisors, reaffirming their long-term objectives.

Learn more about

Our latest insights

-

-

Artificial Intelligence

-

Technology & Innovation

-

-

Demographics & Culture

RELATED INSIGHTS

-

-

Economic Indicators

-

Global Equities

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capitals Express Investments‘s Canadian mutual funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capitals Express Investments. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capitals Express Investments or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. We assume no liability for any inaccurate, delayed or incomplete information, nor for any actions taken in reliance thereon. The information contained herein has been supplied without verification by us and may be subject to change. Capitals Express Investments funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capitals Express Investments. Copyright © 2024 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2024. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

MSCI does not approve, review or produce reports published on this site, makes no express or implied warranties or representations and is not liable whatsoever for any data represented. You may not redistribute MSCI data or use it as a basis for other indices or investment products.

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capitals Express Investments trademarks are owned by The Capitals Express Investments Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capitals Express Investments funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capitals Express Investments, a global investment management firm originating in Los Angeles, California in 1931. Capitals Express Investments manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capitals Express Investments funds offered on this website are available only to Canadian residents.