Global Equities

Categories

U.S. Equities

Value or growth? Both, says veteran portfolio manager

Martin Romo

Martin Romo

May 17, 2021

Value stocks, after seeming to spend an eternity wandering in the wilderness, have captured investor attention this year. For the three months ended March 31, 2021, the Russell 1000 Value Index recorded an 11.26% total return (in USD), far outpacing the 0.94% gain of the Russell 1000 Growth Index. Investors want to know: Will this rotation toward value-oriented shares prove to be a lasting one?

“There can be growing companies that are cheap and cheap companies that grow, so value and growth are not in opposition,” says equity portfolio manager Martin Romo. “We are in a target rich environment, and there are opportunities to invest in fast growing companies as well as classic cyclical companies."

Romo is a portfolio manager on a mandate in the U.S. where he can take a flexible approach to growth, seeking opportunities with classic growth stocks, cyclical stocks and companies in turnaround situations with the potential to generate capital appreciation.

Romo recently sat down with us to share how he is thinking about investing in today’s environment, the pandemic’s long-term impact on industries and what he believes are the most important innovations for the next decade.

Turning point: A cyclical rotation may be underway

Sources: RIMES, Standard & Poor’s. November 6, 2020, was the last business day before the COVID-19 vaccine was revealed to have more than 90% efficacy against the virus in global trials. Data is as of 4/23/21. Values in USD.

Do you expect the recent rally in more cyclical areas of the market to continue?

As a former chemical analyst, I've spent a lot of time thinking through the cyclical implications, and there are clearly some powerful ones. We've got fiscal and monetary policy that's incredibly supportive of the stock market. But as a former cyclical analyst, I'm also a bit cautious. The enthusiasm in the market today for a recovery and a return to normal is quite startling to me.

I think there are some industries like commercial real estate and energy where COVID is a bit of an extinction event for their future fundamentals. To be clear, I don’t think these industries are going away, but the basis for making predictions about the fundamentals of their businesses has forever changed.

Some scientists have long theorized that the extinction of dinosaurs was the result of a giant meteor crashing into earth about 65 million years ago. Whatever the catalyst, dinosaurs did not survive dramatic shifts in the climate, whereas warm-blooded mammals did. Some industries will adapt and thrive after COVID; others may be more like dinosaurs and go into decline.

Do you view the COVID pandemic as an inflection point that will lead to major changes in the way we live and work?

I have spent a lot of time with Capital’s investment analysts trying to figure out how the pandemic will permanently change people’s behaviour and how that might affect the long-term fundamentals of various industries.

What we found is that select companies are using the pandemic as an opportunity to adapt — to be like mammals, not dinosaurs — by using data, technology and analytics that could lead them to a much stronger competitive position and help us address some of the biggest issues we face in the U.S. today.

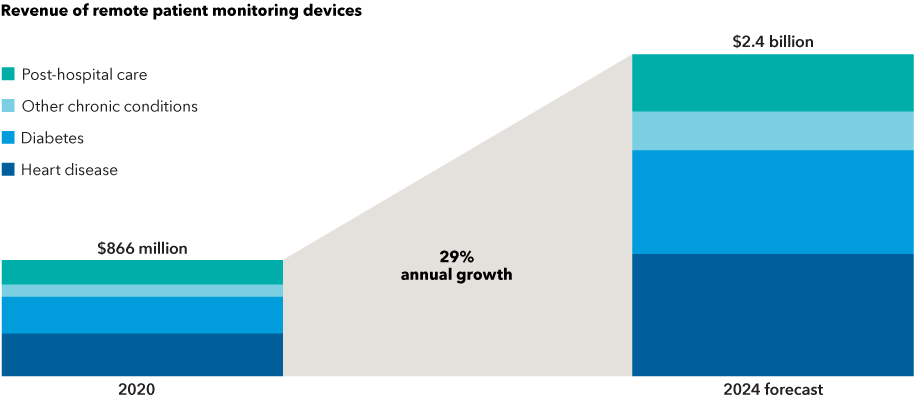

For example, health care is at a big inflection point and is changing for the better. Regulators have relaxed antiquated rules related to “in person” visits, and now doctors everywhere are doing virtual visits. We’re also seeing exciting innovation in wearable monitoring devices — including continuous glucose monitors, insulin pumps, implantable EKG loop recorders and connected sleep apnea devices — that are increasingly enabling physicians to monitor patients remotely.

Wider use of wearable monitors could help improve health care delivery

Sources: Industry & government data, Kagan estimates, Standard & Poor’s. Data compiled June 2020. Values in USD.

Can you share some of your thoughts on the most important innovations for the next 10 years?

I view semiconductors as the single most important innovation of our generation. This innovation stems from World War II, so it’s not new. But like the cotton gin, railroads, electricity, oil and petrochemicals, and mass production, it has the power to drive industrial development for decades. Semiconductors have become central to telecommunications, the internet, data analysis, artificial intelligence, cars and physical products of all kinds.

Since about 1965, the computing power of semiconductors has doubled about once every 18 months to two years — so-called Moore’s law. We're now into cosmic measurements. And that's why it's impacting almost everything we do. As World War II was a leap forward in mass production, COVID, I think, is a leap forward in the capabilities of the semiconductor.

Recent chip shortages are a case in point. Companies can't get enough of them. Auto companies are struggling with their production costs, and countries are starting to say, “This is a strategic resource, and we've got to either develop our own domestic industry or find ways to capture production.”

Take, for example, specialty retailer Williams-Sonoma, which recently said its online sales have surpassed their physical store sales. They are using that leverage to renegotiate lease agreements, changing the economics of their physical stores as their online traffic has increased. They flipped the world from physical to virtual in one year and aren't turning back.

Companies like Mondelez, which spent billions of dollars and a great majority of their advertising budget on TV, are now getting a 25% greater return online and, in fact, 40% better than that if they think about Google and Facebook as their primary ad sources.

And then, in streaming content services, Netflix became the largest content creator in the world at more than US$20 billion spend in 2020.

Semiconductors have enabled this flywheel of innovation and efficiency. The collection of data, the analysis of that data to develop a better product that draws more consumers, whose use generates more data, becomes a virtuous cycle of improvement and wider adoption. It is driving the cost of engagement down and the effectiveness of all our activity higher. And I believe we are still early in this cycle.

Chip suppliers fuel the power behind great products

Sources: Capitals Express Investments, Bloomberg. Data represents semiconductor revenue in 2025, as forecast by Bloomberg, categorized by its end-use product. Estimates are the latest available as of 3/31/21.

What are your thoughts about the growth potential for streaming content and video games?

I remember hours and hours spent on my Atari 2600 when I was 10 or 11 years old. Today’s gamers enjoy unlimited use in an interactive format. Considering the relevance and potential adoption of this form of entertainment by the next generation of consumers, the potential return on the dollar is compelling.

Total global spending on games was up 20% last year to US$180 billion. Keep in mind that the global movie industry peaked in 2019 at US$100 billion. So it's one of these quiet, overnight stories that really isn't overnight, and the thing that's fascinating is that games aren't just participatory. They're spectator sports that are going to take on Broadway and the NBA. Many of these online players collect multimillion-dollar annual contracts in addition to endorsement deals.

Consider that Amazon Twitch, one avenue of spectating, has 1.9 billion hours per month in viewership. That compares to the NFL at 1.65 billion per month. That’s remarkable — and these games are only getting more immersive. There's a company called Roblox that represents a generation of kids — most of them under 15 — who not only are playing in this collective universe with their friends, but they're actually developing games for each other.

The foundation for companies that can leverage these opportunities is profound. So I will watch gaming closely as it continues to encroach on other forms of entertainment.

Streaming entertainment will take centre stage

Source: Capitals Express Investments. Broadway show cost from Jefferies, as of July 2019. NBA ticket cost from Barrytickets for 2018–19 season. Console video game cost from Business Insider, as of October 2018. Video streaming cost is for a standard monthly Netflix subscription as of December 2020.

When do you think life will get back to the “new normal?”

We're in the business of figuring out the “what,” not the “when.” Most of our competitors are looking for the when. When will COVID be over? When will rates go up? Neil deGrasse Tyson is famous for talking about the difference between climate change and weather prediction. And he uses a great example where he's walking his dog on a leash on the beach. He's walking to a flag, and his dog is wiggling back and forth. And he says, "I'm climate change, and the dog is weather prediction." And we have the benefit at Capitals Express Investments of looking forward and looking at elements of climate change that are happening within a company, within an industry, but we also look back to learn lessons from history.

You may be surprised at how much we talk about the principles of Capitals Express Investments's foundation in 1931, and how we still hold those commitments to research, a long-term focus and objective-based investing. We take the responsibility of being stewards of capital for our investors incredibly seriously. We've been here for 90 years, 13 market crashes, 15 recessions, 16 presidents, one world war and now a pandemic. But our principles haven't changed. It's a remarkable testament to the success of the model. To use my earlier metaphor, I like to think we’re more like mammals than dinosaurs, adapting to a changing world while staying true to our fundamental DNA.

Learn more about

Our latest insights

-

-

Artificial Intelligence

-

Technology & Innovation

-

-

Demographics & Culture

RELATED INSIGHTS

-

Global Equities

-

Artificial Intelligence

-

Technology & Innovation

The Russell 1000 Growth Index measures the results of the large-cap growth segment of the U.S. equity universe.

The Russell 1000 Value Index measures the performance of large-cap value segment of the U.S. equity universe.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Unless otherwise indicated, the investment professionals featured do not manage Capitals Express Investments‘s Canadian mutual funds.

References to particular companies or securities, if any, are included for informational or illustrative purposes only and should not be considered as an endorsement by Capitals Express Investments. Views expressed regarding a particular company, security, industry or market sector should not be considered an indication of trading intent of any investment funds or current holdings of any investment funds. These views should not be considered as investment advice nor should they be considered a recommendation to buy or sell.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capitals Express Investments or its affiliates. This information is intended to highlight issues and not be comprehensive or to provide advice. For informational purposes only; not intended to provide tax, legal or financial advice. We assume no liability for any inaccurate, delayed or incomplete information, nor for any actions taken in reliance thereon. The information contained herein has been supplied without verification by us and may be subject to change. Capitals Express Investments funds are available in Canada through registered dealers. For more information, please consult your financial and tax advisors for your individual situation.

Forward-looking statements are not guarantees of future performance, and actual events and results could differ materially from those expressed or implied in any forward-looking statements made herein. We encourage you to consider these and other factors carefully before making any investment decisions and we urge you to avoid placing undue reliance on forward-looking statements.

The S&P 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capitals Express Investments. Copyright © 2024 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

FTSE source: London Stock Exchange Group plc and its group undertakings (collectively, the "LSE Group"). © LSE Group 2024. FTSE Russell is a trading name of certain of the LSE Group companies. "FTSE®" is a trade mark of the relevant LSE Group companies and is used by any other LSE Group company under licence. All rights in the FTSE Russell indices or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indices or data and no party may rely on any indices or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company's express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The index is unmanaged and cannot be invested in directly.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg’s licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

MSCI does not approve, review or produce reports published on this site, makes no express or implied warranties or representations and is not liable whatsoever for any data represented. You may not redistribute MSCI data or use it as a basis for other indices or investment products.

Capital believes the software and information from FactSet to be reliable. However, Capital cannot be responsible for inaccuracies, incomplete information or updating of the information furnished by FactSet. The information provided in this report is meant to give you an approximate account of the fund/manager's characteristics for the specified date. This information is not indicative of future Capital investment decisions and is not used as part of our investment decision-making process.

Indices are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

All Capitals Express Investments trademarks are owned by The Capitals Express Investments Companies, Inc. or an affiliated company in Canada, the U.S. and other countries. All other company names mentioned are the property of their respective companies.

Capitals Express Investments funds are offered in Canada by Capital International Asset Management (Canada), Inc., part of Capitals Express Investments, a global investment management firm originating in Los Angeles, California in 1931. Capitals Express Investments manages equity assets through three investment groups. These groups make investment and proxy voting decisions independently. Fixed income investment professionals provide fixed income research and investment management across the Capital organization; however, for securities with equity characteristics, they act solely on behalf of one of the three equity investment groups.

The Capitals Express Investments funds offered on this website are available only to Canadian residents.